Home Politics Seven Policies For Government to Consider--- 1a. Tackle Structural Deficit and Widen Tax Base through Inheritance Tax

Seven Policies For Government to Consider--- 1a. Tackle Structural Deficit and Widen Tax Base through Inheritance Tax

Red Pill Editorial Team

Posted 7 months ago

0

0

Background and Introduction

Government has balance deficit for 3 straight year by now, with an accumulation of around HKD310 billion deficit. While the government and Financial Secretary project the deficit as short-term, but there is every possibility that the deficit will become structural.

And unlike large economy like the US and China, which can monetized their debt, Hong Kong as a small and completely open economy cannot do the same or raise debt indefinitely, because of three restriction. Firstly the government has to maintain the Linked Exchange Rate System, which means our monetary policies are largely “outsourced” to US FED. Secondly. Secondly Basic Law stipulated that the HK Government must keep a balanced budget, without raising debt. Lastly, the structural government deficit would bring down or use up government reserve eventually and the employment market (as the Government is the biggest employers in Hong Kong) will be dampened and consumer spending tanks.

The crust of the long-term or structural problem is the Government’s narrow tax base. The government has talked about widening tax base for two decades by now. It comes up with some proposed policies such as sales tax, but all of them are considered complicating the tax code and are regressive in nature (i.e. the poor pay for a larger % of their income that the rich do).

Financial Secretary Paul Chan has stipulated three criteria for widening the tax base or raising the revenue while decreasing the expenditure: 1) It must not interfere with the living of the mass. 2) The rich or the able should pay more for the poor or the not able, which implies that users pay for their expense 3) It must not compromise Hong Kong competitiveness i.e. a simple tax code. But we note that these three criteria are kind of an impossible trinity, so fulfilment of one criteria will often compromise the other. So the question is not to fulfil fully these three criteria but to compromise them as little as possible.

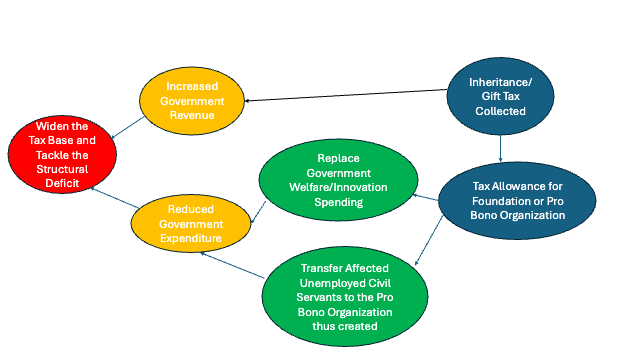

We believe that a resumption of inheritance tax (gift tax), which was abolished in 2006 to simplify the tax code, should be recovered. It broaden the tax base and violate the least of the tri-criteria. First it affects the mass public the least since it targets at the richest population in Hong Kong. Second, obviously, the rich pay more. Third, it does complicate Hong Kong’s tax code a bit, thereby compromising a little of Hong Kong’s competitiveness. But I note that the gift tax will only affect the richest of the residents and most of the talents that are attracted to Hong Kong come from the middle-class. On balance it compromises the tri-criteria.

I note that the government is rolling out other more petty measures to reduce expenditure and raise revenue. Most of such measures involve cutting welfare spending (thus affecting the masses) or increasing service fee (again affecting the masses), let alone the fact that they are petty measures that are short-term in nature and are inefficient in reducing deficit. On the other hand, inheritance tax addresses the long-term and raise far more substantial government revenues.

Implementation: The Public-Private Partnership and Positive Feedback

I suggest the government begins the tax bracket from estates of HKD300million onwards as the definition of middle class is HKD1million to HKD300million (excluding the self-occupied property) so that it only aims at the rich class and does not add burden to the middle class or the lower class. The suggested tax brackets are listed below:

Asset Values (HKD) Tax Percentage Estimated Number of People in this Bracket*

300milllion 15%

1billion 20%

5billion 25%

10billion 30%

*pending government statistics on the wealth distribution of Hong Kong

Most importantly, there is a tax allowance of up to HKD50million given to the inheritance tax payer if they set a pro bono organization (like the Tung Wah Group) or foundation (like the Our Hong Kong Foundation). It will reduce government expenditure on welfare in the long-run and almost permanently. Furthermore, I suggest the civil servants thus cut by the less welfare-related personnel need will be given priority to work in the pro bonos thus created. This will trim government expenditure too.

In summary, such tax allowance is a form of public-private partnership that the government has been advocating for a decade now. It simply transmit the government expenditure on welfare and related civil servant to the private sector (pro bono organization), which is kind of the relics of “smaller government and larger private sector).

0

0

Popular Tags

Popular Articles

Copyright ©2025 Fortress Hill Media limited. All rights reserved